| ||||

Between 2014 and 2016, The Southern Tier West Regional Planning and Development board surveyed farmers market customers in Allegany, Cattaraugus, and Chautauqua counties situated in the southwestern most part of New York State. The counties do differ in size as Cattaraugus is almost twice the size of Allegany; Chautauqua is almost three times as large as Allegany county. Still, the region across each individual county is plagued by rural poverty and a declining population. Given the exodus of young men with high earning potentials, the population of The Western Southern Tier is largely older, lower-income and more female on average.

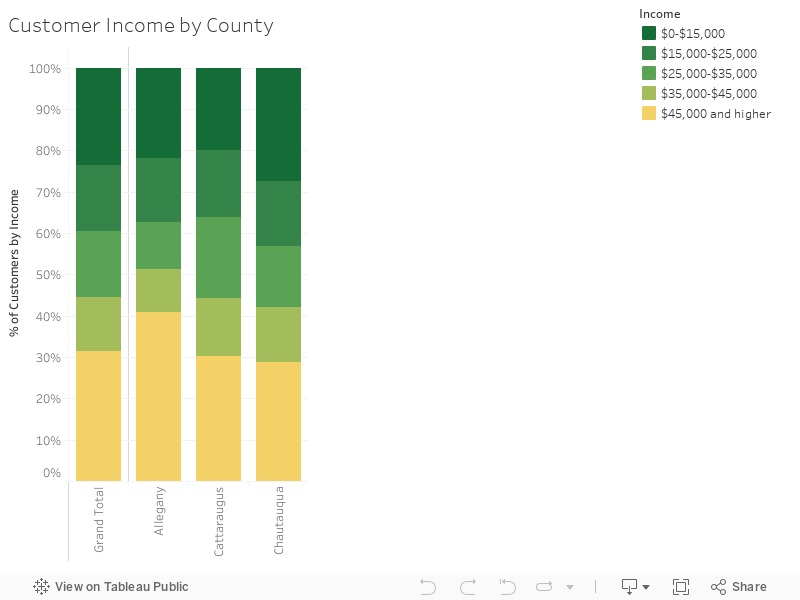

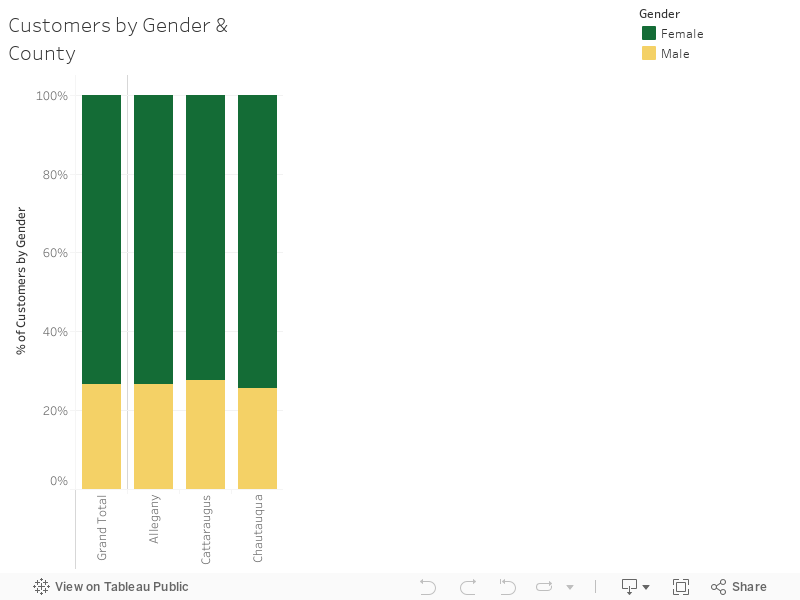

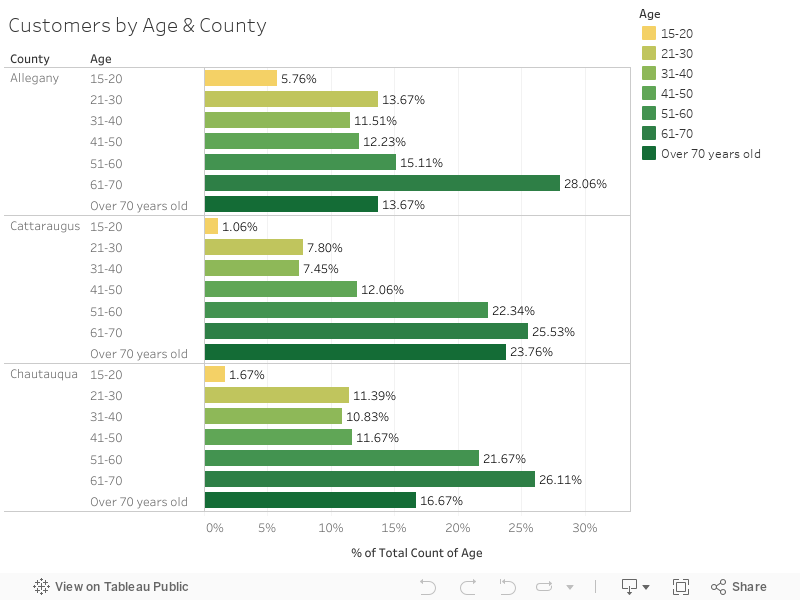

Thus, on the one hand, the mostly older (44.94% are over the age of 60), lower-income (only 31.5% make more than $45,000 annual) and largely female (73.5% are women) clientele of the farmers markets in the region is fitting with the larger population characteristics. Yet on the other hand, comparative data reveals how the market customers are so predominantly older, lower-income women that the primary room for expansion is into younger, higher-earning men. Fortunately, the survey data also reveals the best ways to target this new group of potential customers.

Also, in being aggregated at the county level and above, this report only outlines broad trends and considerations generalized to The Western Southern Tier region. Prior to taking any actions, managers should consider obtaining a market-specific report from Southern Tier West on more recently collected data.

Thus, on the one hand, the mostly older (44.94% are over the age of 60), lower-income (only 31.5% make more than $45,000 annual) and largely female (73.5% are women) clientele of the farmers markets in the region is fitting with the larger population characteristics. Yet on the other hand, comparative data reveals how the market customers are so predominantly older, lower-income women that the primary room for expansion is into younger, higher-earning men. Fortunately, the survey data also reveals the best ways to target this new group of potential customers.

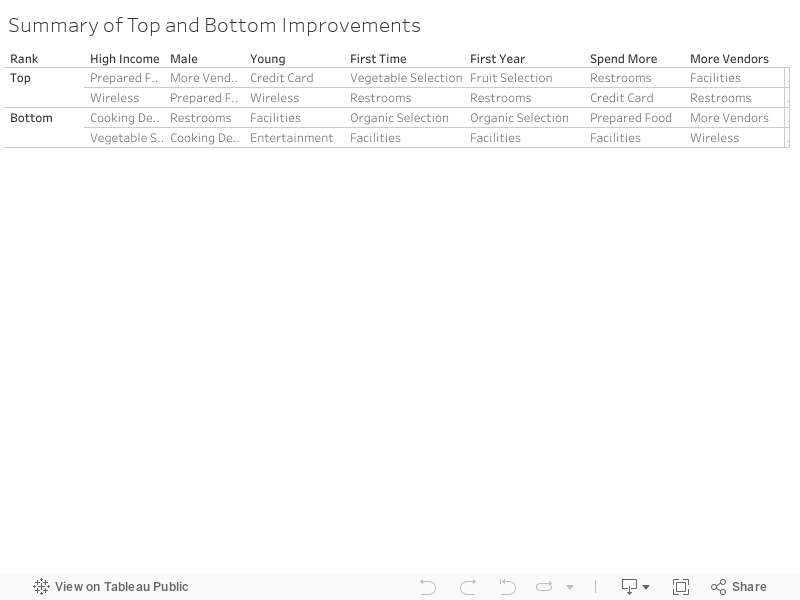

- The largest proportion of shoppers earning more than $45,000 come to the market to support local agriculture (40.43%). Over half heard about the market via the internet (53.33%), and over half of shoppers purchased eggs (53.85%), meat, poultry, fish (51.52%), dairy and cheese (50%). They mostly thought adding a wireless internet network would improve the markets (42.86%), followed by an interest in expanded selection of prepared foods (37.84%).

- In coming to the market primarily because of freshness and taste (36.32%), men were most likely to purchase maple (44%) and honey products (31.03%). More than any other means, almost a third (32.65%) heard about the market through the media. More prepared food (32.23%) was the most frequently cited improvement made by men.

- Drawn to the market to support local agriculture (41.36%) and compelled by a WIC/SNAP referral (66.67%), customers under thirty years of age were most likely to purchase juice (50%) and packaged foods (30.77%). Wireless access (25%) was the most common cited improvement made by those under thirty, followed by the ability to pay by credit card (21.18%).

- Maple is the most common product purchased by first-time visitors (17.86%), who are drawn to the market primarily because of freshness and taste (37.11%). Almost half (44.44%) were referred to the farmers market by WIC or SNAP. The most common improvement suggested by those at the market for the first time is access to onsite restrooms (16.13%).

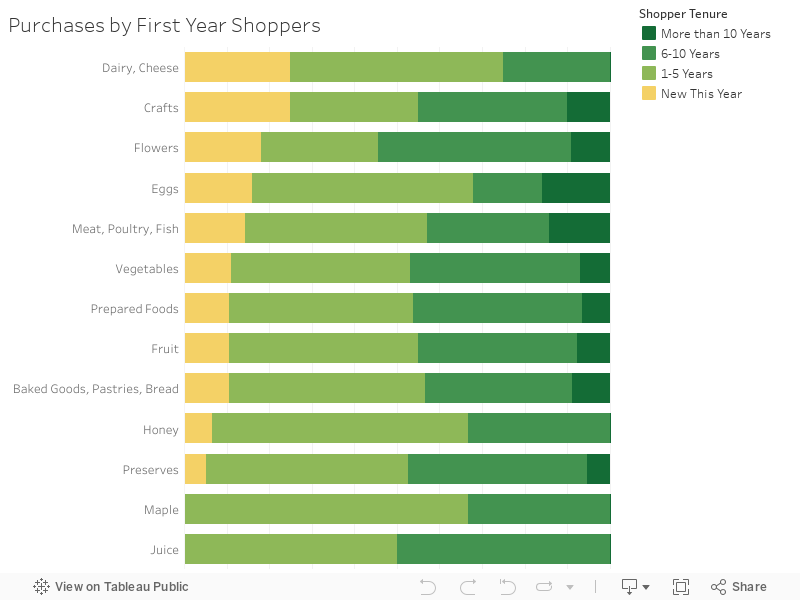

- Over half (51.28%) of first year shoppers come to the market for freshness and taste. A quarter (25%) of first-year visitors purchased crafts along with dairy and cheese. Over two-thirds (66.67%) were referred to the farmers market by WIC or SNAP. More than any other improvement, first-year shoppers said restrooms (28.57%) would enhance the farmers market.

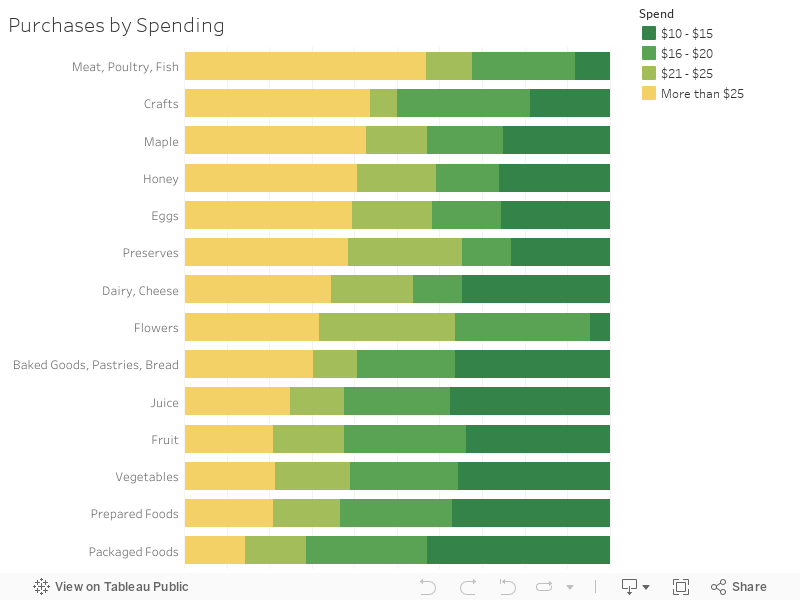

- Over half of those who spent more the $25 at the market (56.76%) purchased meat, poultry or fish. Supporting local agriculture (40.22%) was the most common reason stated for shopping at the farmers market. The largest proportion (17.65%) heard about the market via the internet. These highest-spending customers called for the ability to pay with credit card (19.77%) and restrooms (19.35%) as the primary ways to improve the market.

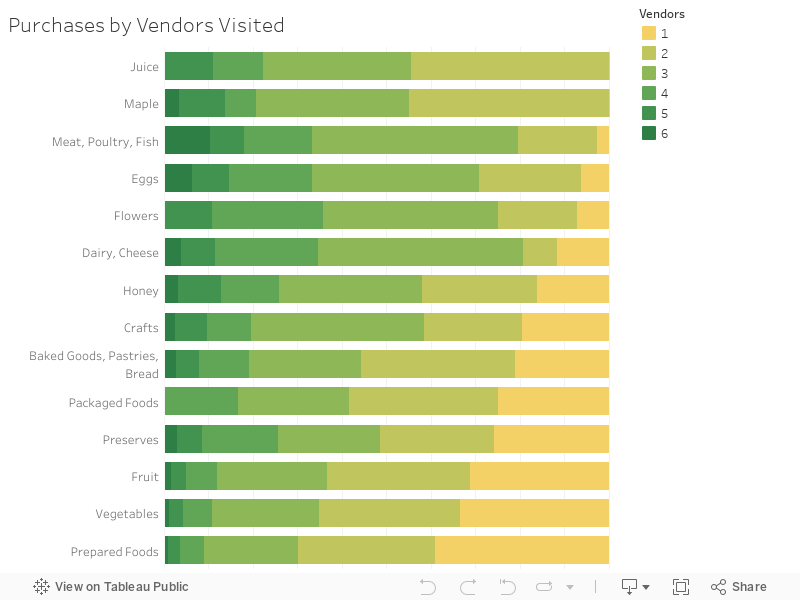

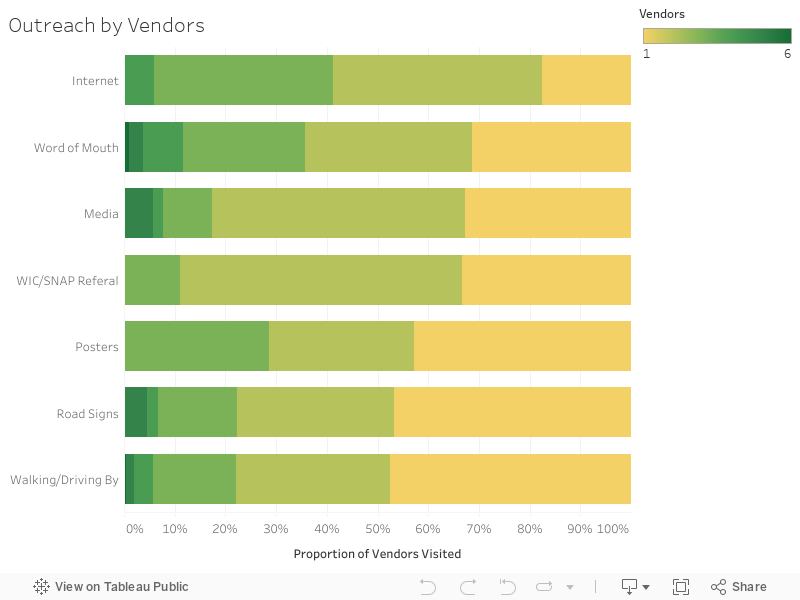

- Everyone who purchased juice or maple products visited more than one vendor at the market. Shopping with more vendors was significantly correlated with support for local agriculture and hearing about the market via word of mouth. These shoppers were also significantly more likely to call for an extension of the market season.

Also, in being aggregated at the county level and above, this report only outlines broad trends and considerations generalized to The Western Southern Tier region. Prior to taking any actions, managers should consider obtaining a market-specific report from Southern Tier West on more recently collected data.

Between 2014 and 2016, The Southern Tier West Regional Planning and Development Board (STW) administered 822, twenty-question surveys to a random sample of customers at farmers markets across the southwestern most counties of New York State. According to the 2016 5-Year Estimates from the American Community Survey, Chautauqua was the most populous county in The Western Southern Tier with a population of 131,748. All but one of the markets (Westfield) were in one of the two major population centers of Jamestown (including the suburbs of Lakewood and Falconer) or Fredonia-Dunkirk. Cattaraugus county had a population of 78,506 in 2016, and two of the six markets were in the population of center of Olean. There are no cities in Allegany County, which had a 2016 population of 47,700, and thus all of the markets operate in small villages. Although the populations sizes vary across the three counties, all are predominantly white, have aged populations on average, and face challenging socio-economic conditions like high poverty rates and a declining population stemming from deindustrialization.

While the surveys were originally conducted for individual market reports, the aggregated results provide an unprecedented opportunity to develop general strategies to expand markets’ customer base throughout The Western Southern Tier.

|

Demographics

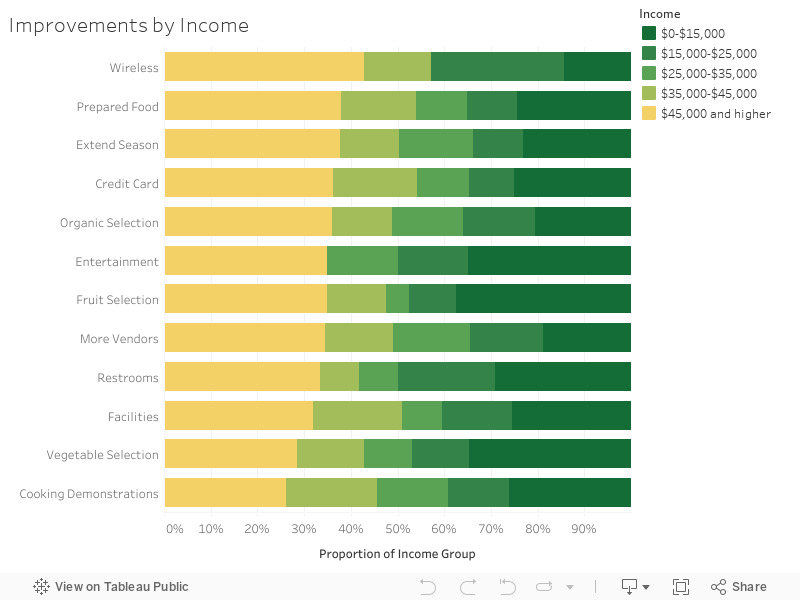

Across The Western Southern Tier, over two-thirds (68.5%) of consumers at farmers markets make less $45,000 annually. Regionally, the median income is $43,572 according the 5-Year Estimates from the American Community Survey. The largest proportion of shoppers with incomes of $45,000 and higher is in Allegany county (40.87%) while the lowest is in Chautauqua where over a quarter of customers (27.43%) make less than $15,000. Thus, even though the region is socioeconomically distressed, farmers markets serve those with lower than average incomes in the area. This means there is room for Western Southern Tier farmers markets to expand their customer base into higher income clientele who may, with more resources at their disposal, spend more. |

|

The low incomes of Western Southern Tier farmers’ markets shoppers do not appear to be from widespread use of nutrition programs such as SNAP, WIC or Senior Coupons, since this reflects only 1 in 5 customers (20%) across the region.

|

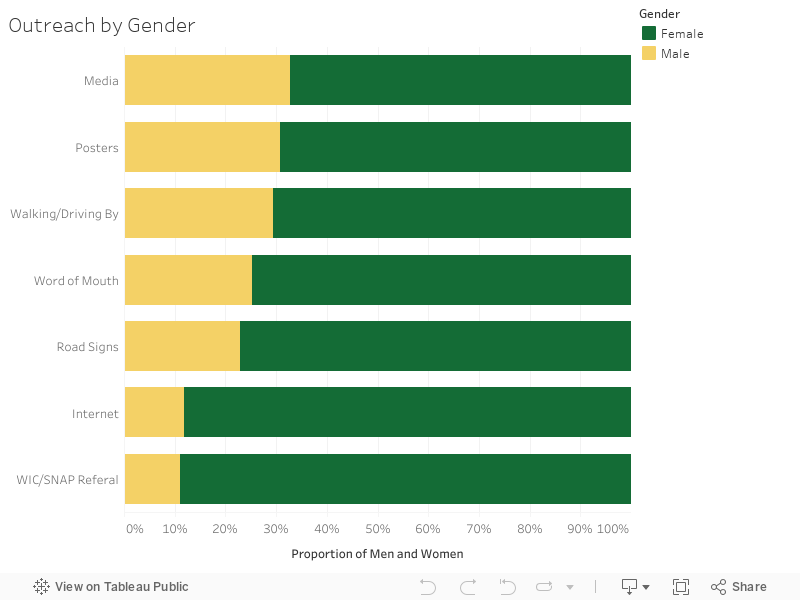

With only 98.51 males per female across The Western Southern Tier in 2016 (see the 5-Year Estimates of the American Community Survey), there are more women than men across the three counties. Yet even with this regional difference, farmers markets in The Western Southern Tier serve many more women than male customers comprise almost three-quarters (73.5%) of clientele. Thus, even though there is an imbalance of the sex ratio in Allegany County compared to the rest of region, the gender makeup of farmers market customers varies little across the three counties where 73.5% of customers are women. This means across The Western Southern Tier men may be an untapped customer base of regional farmers’ markets. Changing times means future surveys might also reconsider reducing gender to a binary variable.

|

|

According to the 5-Year Estimates of the 2016 American Community Survey, with a median age of 41.2 the Western Southern Tier has an older-than-average age compared to New York State (38.2) and the nation as a whole (37.7). Still, only 7.92% of Southern Tier Citizens are over seventy years of age, yet 17.84% of market customers are of this age.

Thus, markets across The Western Southern Tier could consider outreach to younger customers to expand their clientele.

Shopping Patterns

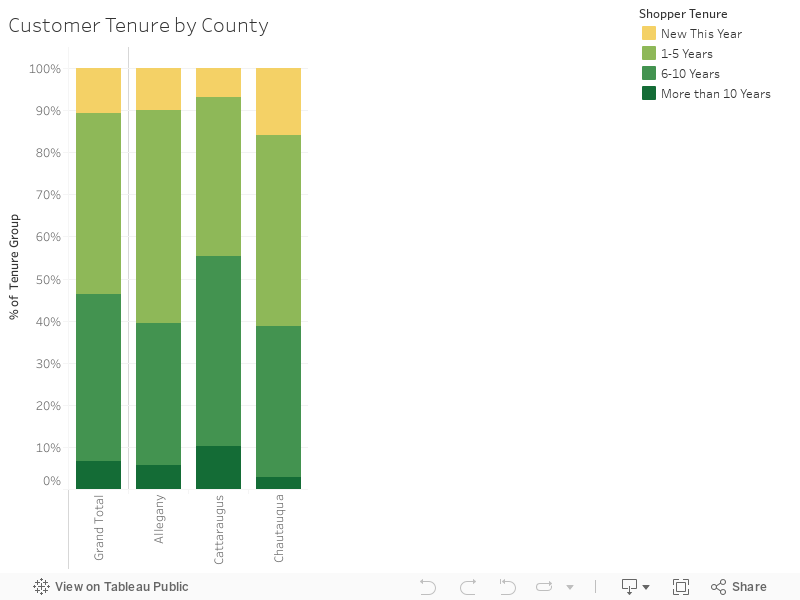

Customer tenure, frequencies of market visits, typical spending, and vendors visited was assessed amongst the older, mostly female and lower-earning customer base of Western Southern Tier farmers markets.

Customer tenure, frequencies of market visits, typical spending, and vendors visited was assessed amongst the older, mostly female and lower-earning customer base of Western Southern Tier farmers markets.

|

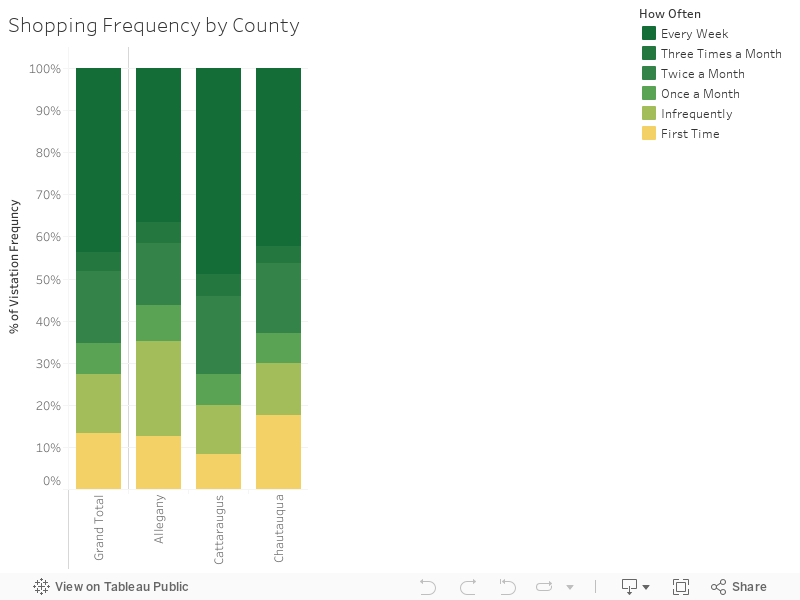

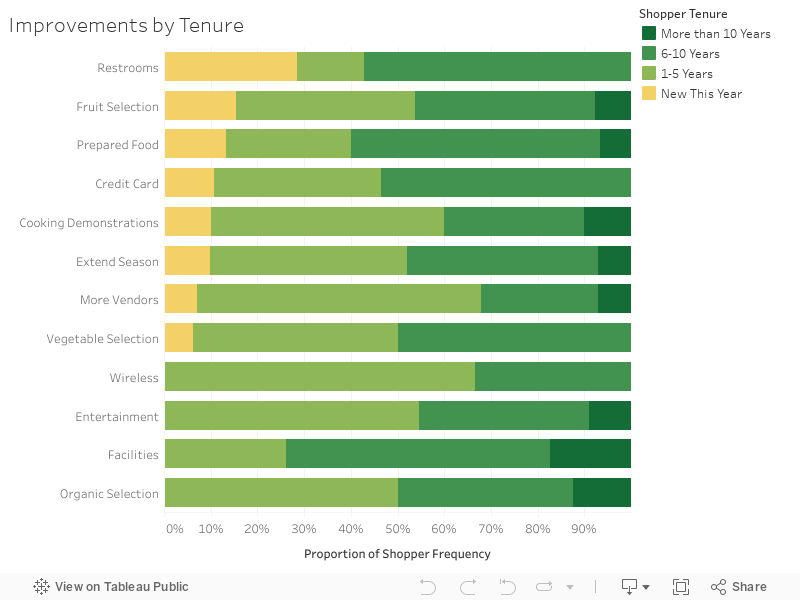

Chautauqua County has the largest proportion of first year shoppers (15.86%), while Cattaraugus County has the fewest (6.78%). With only 10.7% shoppers coming for their first season across the region, most patrons are long-term customers. Impressively, 6.62% of farmers market shoppers in the Western Southern Tier have been coming to their marker for over a decade. However, the largest proportion of shoppers (43%) have frequented the market of between one and five years.

The question for regional farmers markets is how to ensure those coming to the market for their first season shop in subsequent years, thereby transitioning into long-term customers. In fact, answering this question is a primary objective for this report. This answer of course takes on a sense of urgency with the accelerated age of the typical farmers market customer.

|

|

|

Most shoppers surveyed are best described as “regulars,’ almost half (43.6%) visit the market every week. There are variations across the counties, however. Almost half of farmers market customers in Cattaraugus County (48.95%) visit every week compared to just over a third (36.92%) in Allegany county. Chautauqua county has the largest proportion of First-time visitors (17.5%) while Cattaraugus has the fewest (8.39%). With the exception of Allegany county, the proportion of infrequent visitors (22.54%) remains low across the Western Southern Tier (13.91%).

This frequency of visitation data can be further analyzed and utilized to see what changes could be made to turn infrequent visitors into frequent ones, largely by ensuring the 13.41% of first time shoppers return.

|

|

|

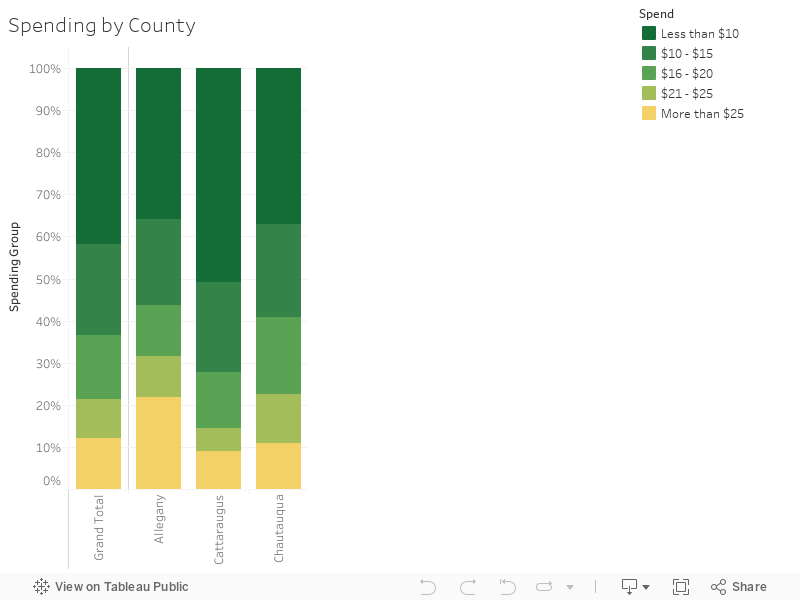

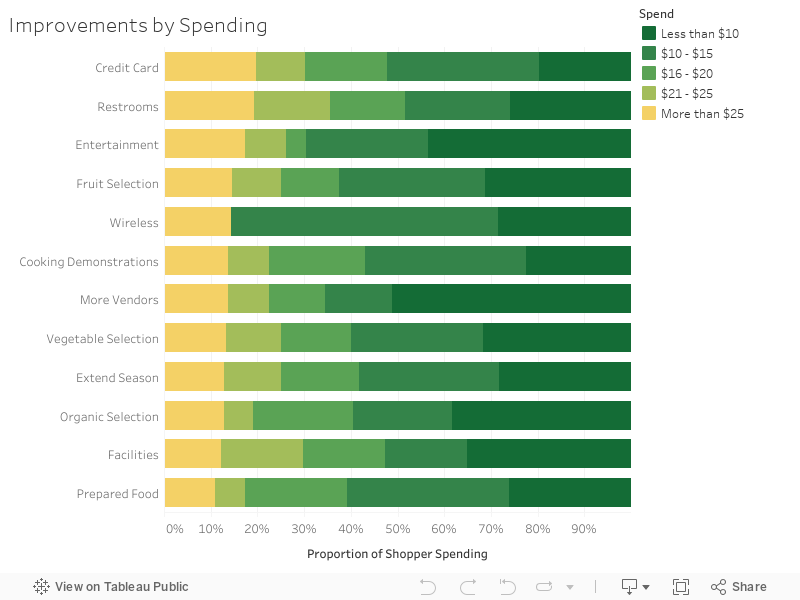

Even while considering markets are frequented largely by those with limited incomes, spending remains lower across the region than what would be anticipated given the cost of a healthy diet as almost two-thirds (66.3%) of patrons spend less than $15. Only 12.22% of farmers market customers spend more than $25. Allegany county has largest proportion of customers spending more than $25 (21.83%) and the smallest number of shoppers (35.9%) spending less than $10. Over half the shoppers in Cattaraugus County (50.88%) spend less than $10 at the farmers market.

|

|

|

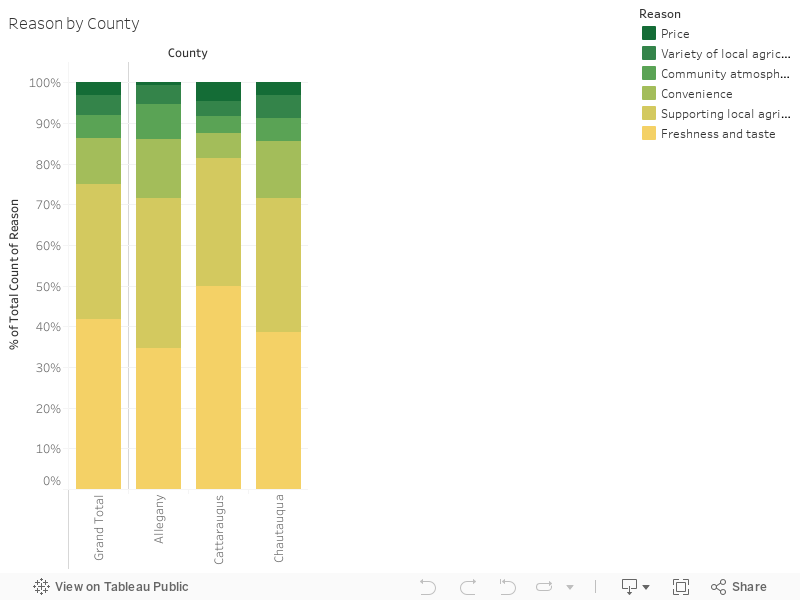

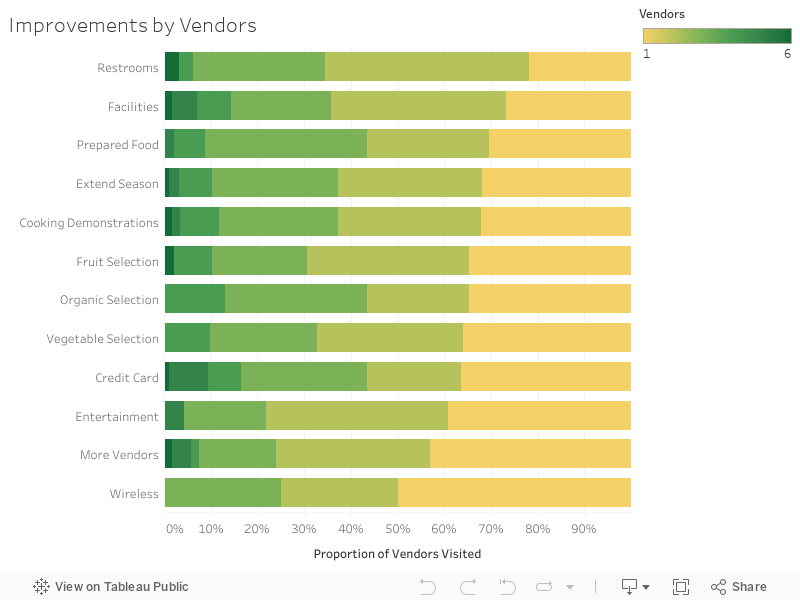

Low spending is somewhat surprising as price is, in fact the very last reason why shoppers frequent a market (3.1%). Rather, the largest proportion of consumers said the number one reason they shop at farmers markets are freshness and taste (41.9%), followed by support for local agriculture (33.2%). Furthermore, generally low levels of spending can be partially explained in how almost forty percent (39.1%) of customers only purchase from a single vendor; over two-thirds (69.9%) secure products from two or less vendors.

Thus, further analysis will detail what types of customers spend the most from the most vendors.

|

|

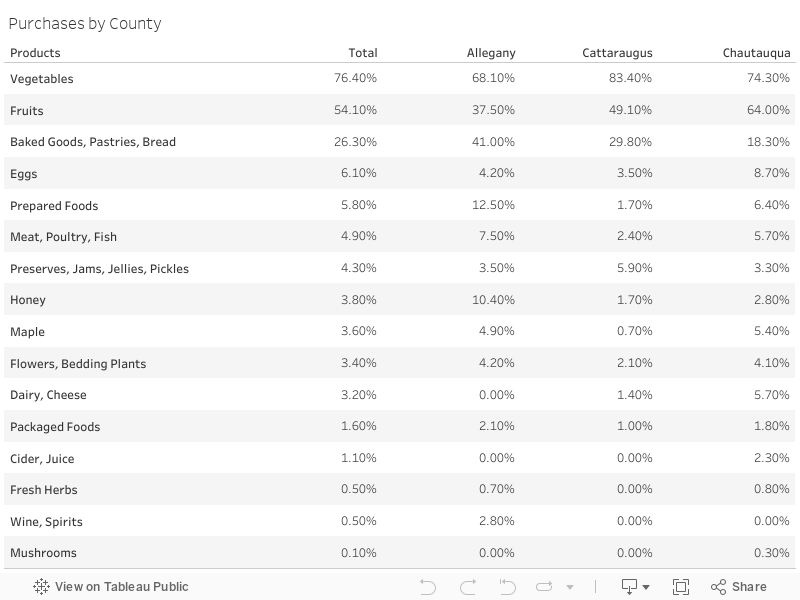

Customers were asked what they purchased and this data can be utilized to assess which products could be promoted in order to attract underserved and/or idealized customers—mainly younger, higher-income men who spend more money, with more vendors who hopefully can be drawn from both first-time market visitors or those coming to the market their first season.

Unfortunately, the few customers purchasing mushrooms (.1%), fresh herbs (.5%) and wine/spirits (.5%) makes further analysis infeasible for these product categories. Still, the purchases of most products can be cross tabulated with demographic and shopper characteristics to reveal what under-served and/or ideal customers buy the most, and the least.

Unfortunately, the few customers purchasing mushrooms (.1%), fresh herbs (.5%) and wine/spirits (.5%) makes further analysis infeasible for these product categories. Still, the purchases of most products can be cross tabulated with demographic and shopper characteristics to reveal what under-served and/or ideal customers buy the most, and the least.

Demographics

The income, gender and age of shoppers cross tabulated with purchases reveal what underserved customers across the region purchase at farmers markets.

The income, gender and age of shoppers cross tabulated with purchases reveal what underserved customers across the region purchase at farmers markets.

|

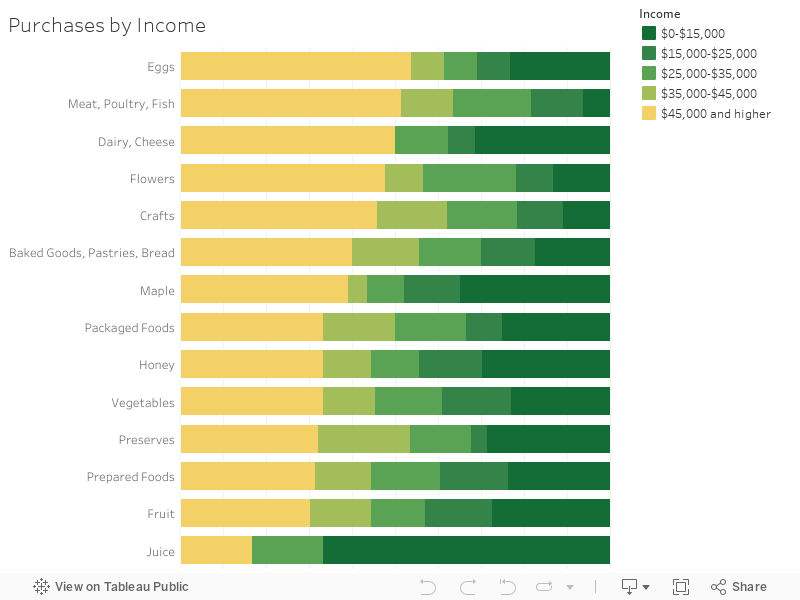

Across The Western Southern Tier, most farmers’ market shoppers earn less than the median salary of the region (which is depressed relative to both New York State and the nation as a whole). Still, comparing current farmers market customers with the incomes earned across the counties (and region) affirms that markets could expand their customer base by ensuring they offer the products higher-earning clientele desire. According to the data, those making over $45,000 are unlikely to purchase juice, fruits and to a lesser degree, vegetables. Instead of market staples, higher-income shoppers gravitate towards meat, poultry, and fish along with eggs, dairy and flowers. Instead of market staples, higher-income shoppers gravitate towards meat, poultry, and fish along with eggs, dairy and flowers.

|

|

|

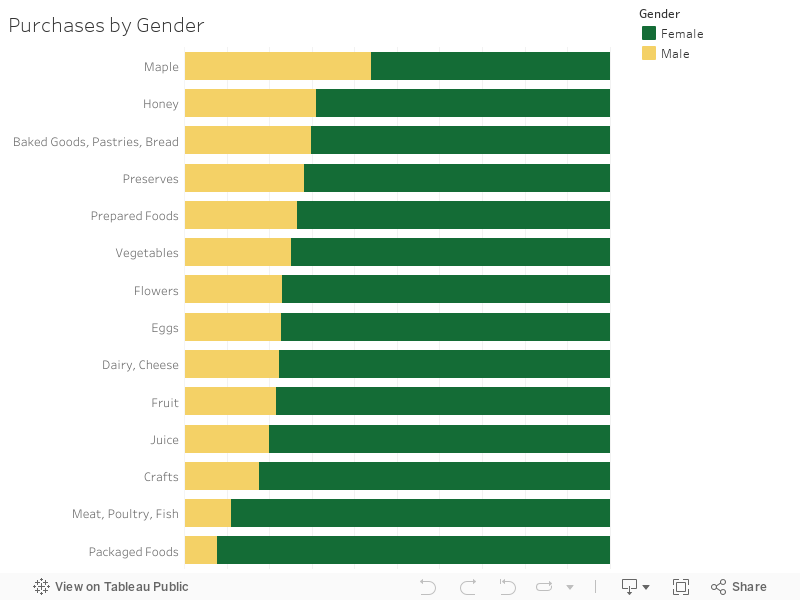

While there are fewer men than women across The Western Southern Tier, since almost three-quarters of farmers market customers are women, men are an untapped customer base across the region. Somewhat in contrast to stereotypes, men are unlikely to purchase meat, poultry and fish; they are only less likely to purchase packaged foods. Rather, men are more likely to purchase maple, honey and baked goods like pastries and bread. In terms of market staples, a little over a quarter of men (25.13%) purchased vegetables while 21.67% bought fruit.

|

|

|

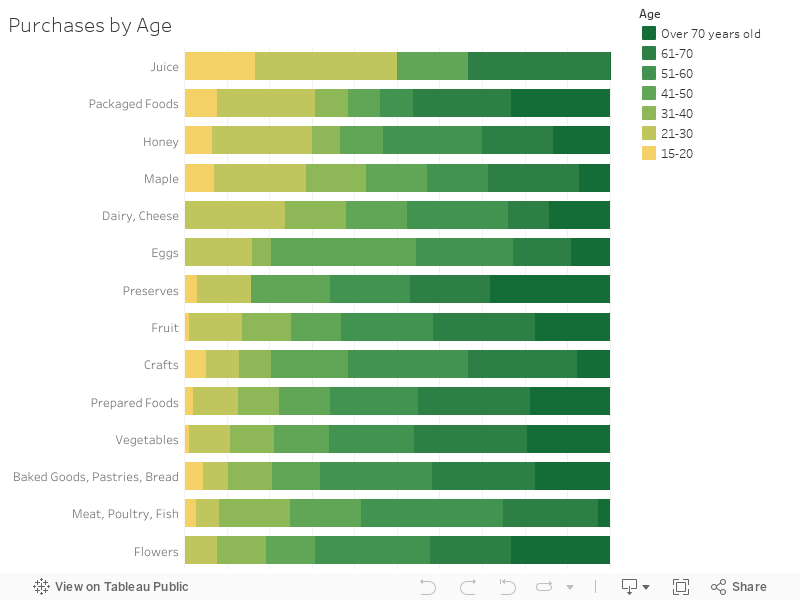

Perhaps more so than other demographics, for long-term survival it is especially important for farmers markets to expand into young demographics. Similar to men, those under 30 are unlikely to purchase meat, poultry and fish; the only product they are less likely to purchase is flowers. Perhaps because they tend to have young children, those under 35 are especially likely to purchase juice; followed by honey and maple products, which are also popular amongst those with higher incomes. Customers under 30 are the only demographic group more likely to purchase fruit over vegetables.

|

|

Unfortunately, there is not a single product category that appeals to all underserved demographic groups markets could not only offer, but also situate within in a market to ensure targeted groups pass by other vendors. High-income patrons are attracted to meat, poultry and fish; yet these are unlikely to be purchased by young men. Younger customers are drawn to juice; but this is the least likely purchased by higher income patrons. Thus, the community demographics could be utilized to pick the best products to offer and strategically place. For instance, the only county in The Western Southern Tier to have more women than men is Allegany, thus markets here might want to focus on attracting young, higher-earning customers—especially when also considering this county has the lower median age and highest median income across the region. In contrast, Chautauqua county is the oldest and poorest, thus markets located in this western most part of the region may want to focus outreach efforts on men. Of course, community specific reports would provide the most accurate local data for planning.

Shopping Patterns

Given that most farmers market shoppers are long-term customers, care should be taken to ensure first-time and first-season visitors return by ensuring markets offer what these clients seek—especially if these customers also spend large amounts of money, with a large number of vendors.

|

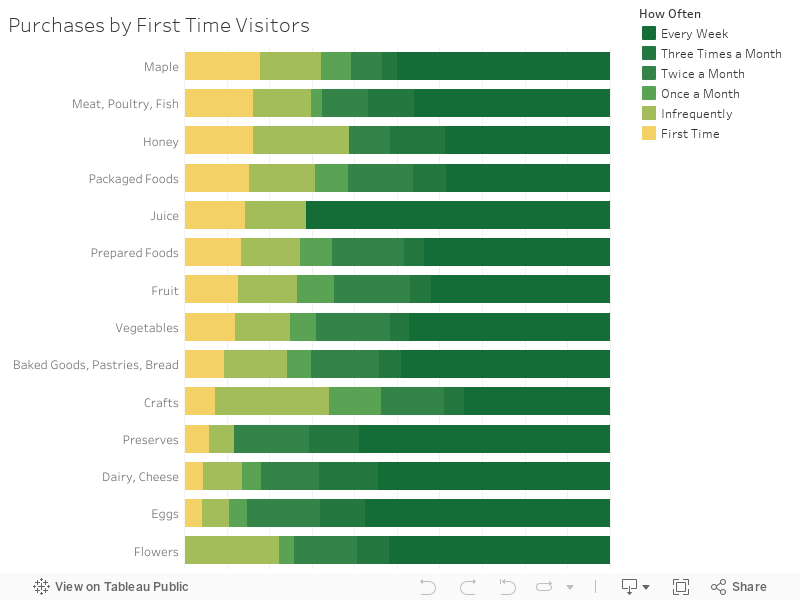

It is important to know what first-time visitors purchase in order to secure their return to future markets. According to the cross tabulation, first time visitors are the most likely to buy maple and honey, along with meat, poultry and fish. Nobody purchased flowers on their first visit to the market; very few bought dairy, cheese or eggs. First time visitors were slightly more likely to purchase fruits (12.76%) than vegetables (11.97%).

|

|

|

By analyzing what they do and do not purchase, efforts can be made to ensure those coming to the market for their first season return in subsequent years. No first-year customers purchased juice or maple or dairy products, and very few bought honey or preserves. Rather, first year shoppers are more likely to purchase dairy, cheese, crafts or flowers. About the same percentage (10%) of first season customers purchased fruits and vegetables.

|

|

|

Ideally, a high-spending customer is financially equivalent to two or more less-spending customers; thus, attention should be paid to the products that maximize spending. Over half of those spending more than $25 bought meat, poultry or fish; followed by crafts, then maple and honey. Those who spend the most at the market are the least likely to purchase prepared or packaged foods, followed by the market staples of fruits and vegetables.

|

|

|

Customers who visit a large number of vendors are ideal. According to the cross tabulation, nobody purchasing juice or maple were exclusive to a single vendor; and most purchasing meat, poultry or fish also secured products from another provider. Nearly identical to the pattern observed with those who spent more than $25, a large proportion of those who frequent more vendors are less likely to purchase prepared foods. The data also reveals those shopping primarily for market staples (fruits and vegetables) seem exclusive to just a few vendors.

|

|

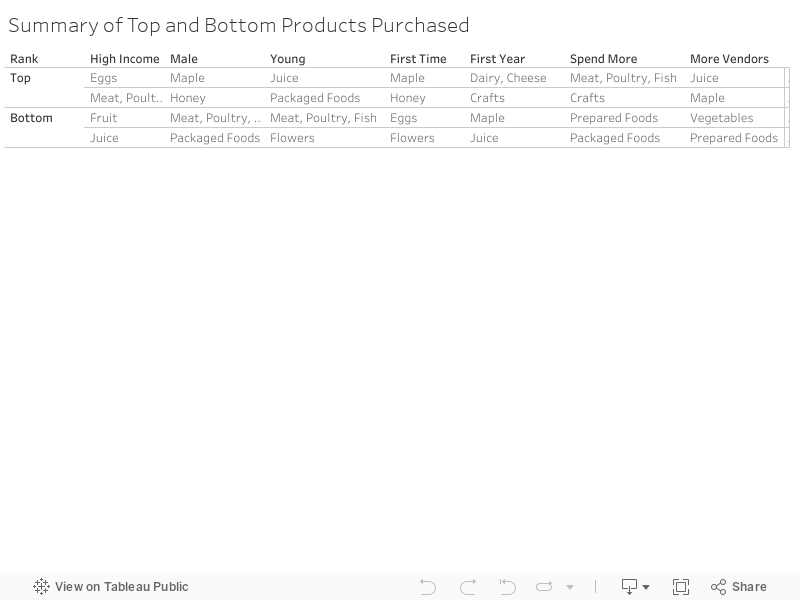

The data shows that first time customers are the most likely to purchase maple and honey, which unfortunately is the least likely products to be purchased by those coming to the farmers market for their first season. Instead, first-season clientele gravitate toward dairy products and crafts. Fortunately, there is an overlap with meat, poultry and fish between those spending more and those who visit multiple vendors. The top and bottom two products purchased across underserved demographic groups and ideal shoppers can reveal the best, and worst farmers market offerings. Three products appear three times in the top category; maple, crafts, along with meat, poultry and fish—the latter of which unfortunately appears twice on the bottom list along with flowers. However, the least common products purchased by underserved and less-ideal customers are packaged and prepared foods.

Knowing the primary motivation customers have for shopping at farmers markets is the first step in developing effective outreach and promotion to new customers. The data reveals that mainly the young, upper-income men underserved across The Western Southern Tier will come to the market and spend more, at more vendors. Ideally, these customers could be drawn from those visiting for the first time, or for their first season.

|

Demographics

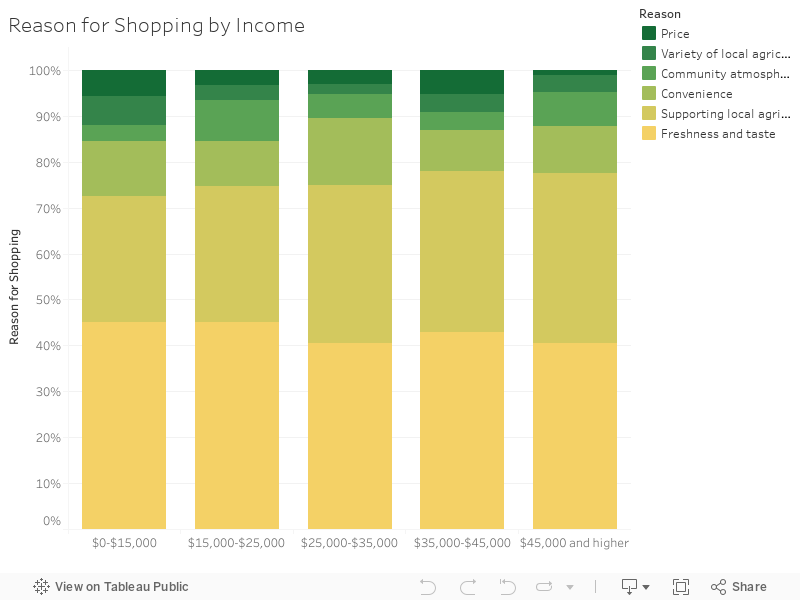

Higher income clientele are underserved by The Western Southern Tier farmers markets and this is troubling assuming these would be the same customers who would spend more money, with more vendors. While price is not a concern for shoppers generally; it is even less of a concern for those who with heightened incomes who are an untapped demographic for Western Southern Tier farmers markets. The most common reason that those who make more the $45,000 shop at the market is for freshness and taste, although they are less likely than any other income group to shop for this reason. Rather, they are more likely than any other income group to frequent farmers markets to support local agriculture. Price and variety of local agricultural products are the least likely reasons why those with heightened incomes shop at farmers markets.

|

|

The most common reason that those who make more the $45,000 shop at the market is for freshness and taste, although they are less likely than any other income group to shop for this reason. Rather, they are more likely than another other income group to frequent farmers markets to support local agriculture. Price and variety of local agricultural products are the least likely reasons why those with heightened incomes shop at farmers markets.

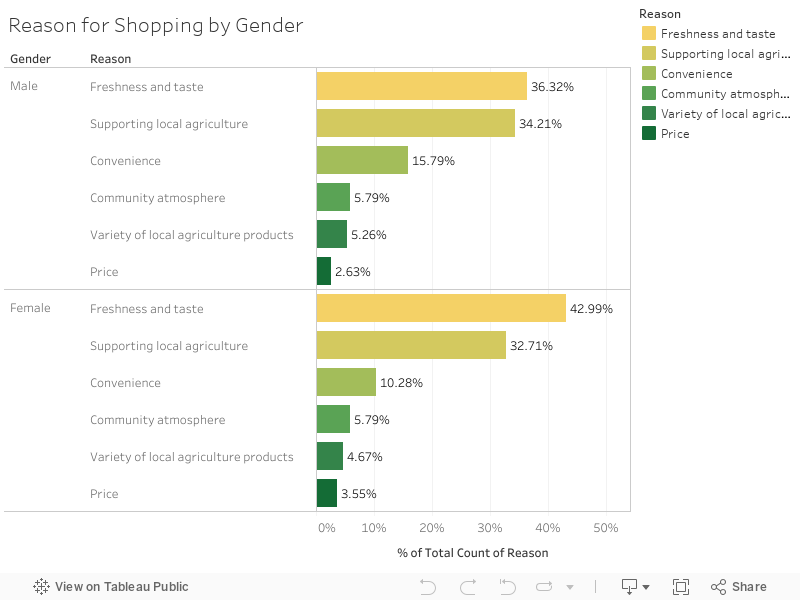

Men are the largest demographic group undeserved by farmers markets. Like those with heightened incomes, men are more likely than women to frequent farmers markets to support local agriculture.

Men are the largest demographic group undeserved by farmers markets. Like those with heightened incomes, men are more likely than women to frequent farmers markets to support local agriculture.

|

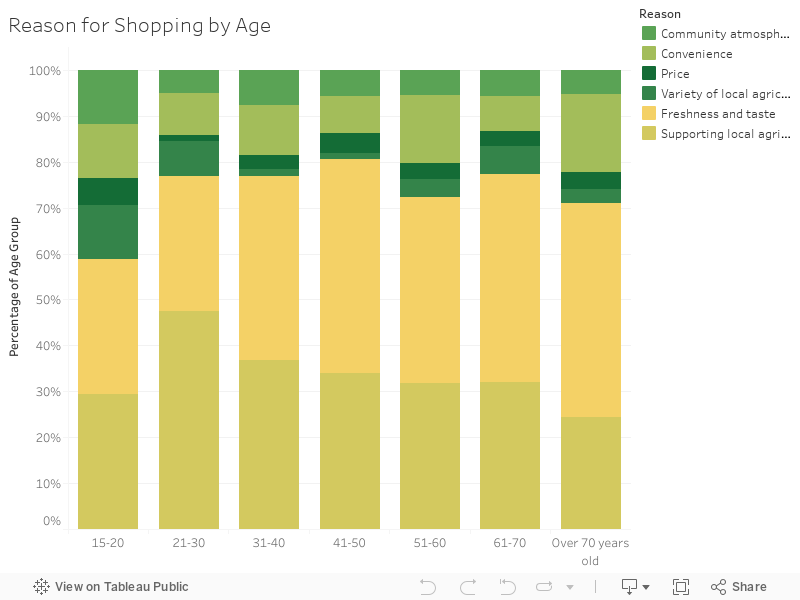

Similar to higher earning men, those under thirty are more likely than their older respondents to say they shop at farmers markets to support local agriculture. Young customers are less likely than older shoppers to claim freshness and taste as their primary motivation for frequenting the market. As with other demographic groups, price along with a variety of agricultural products are low ranking reasons to shop at farmers markets.

|

|

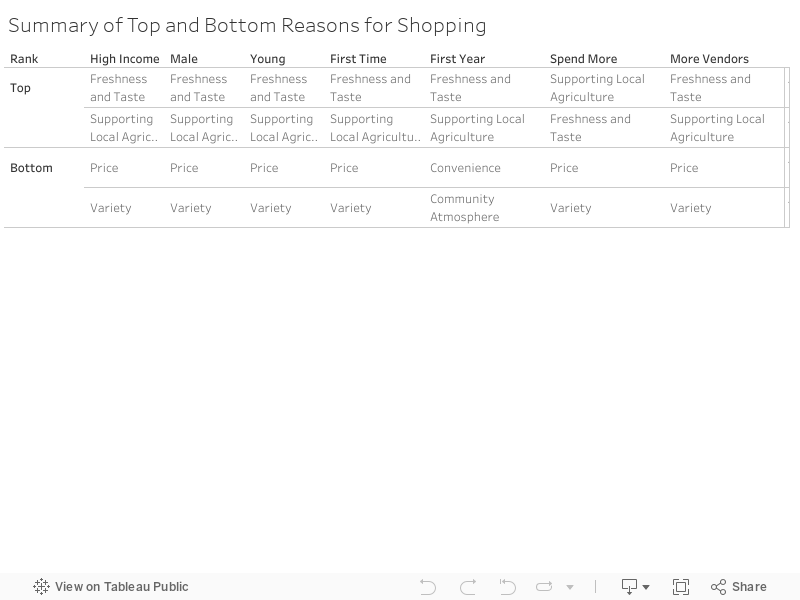

Thus, a consensus emerges across demographic groups as all underserved factions, mainly young, high-income men frequent the farmers market primarily for freshness and taste, followed closely by support for local agriculture, and this could be the basis of promotion. In contrast, the data show outreach on the basis or price of variety are unlikely to attract younger, higher-spending men.

|

Shopping Patterns

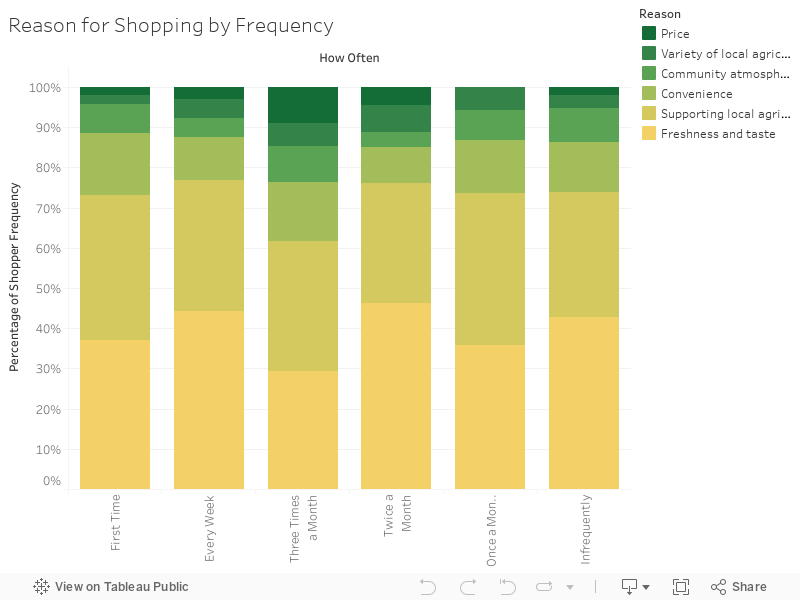

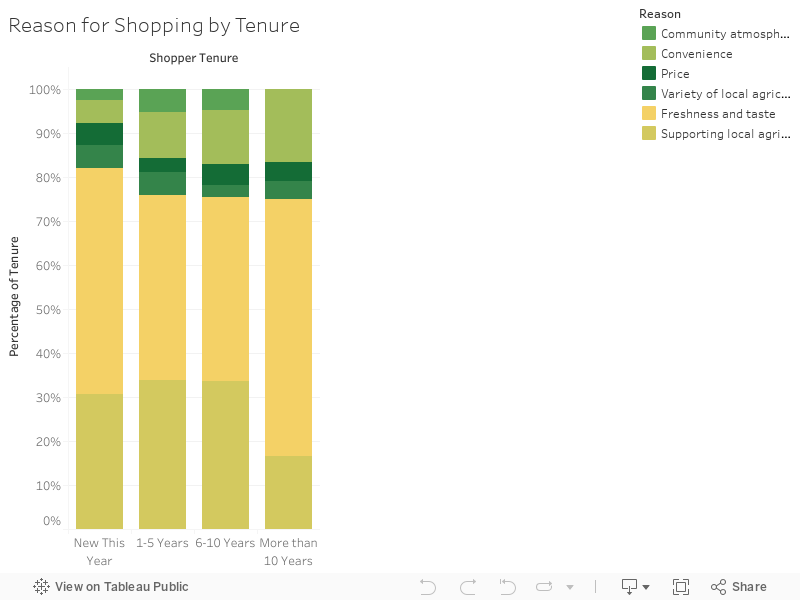

Proper promotion holds promise to turn first time and first year visitors into long-term customers who spend more, with more vendors. According to the data, first time visitors are more likely than most others who visit more regularly to say they frequent the market to support local agriculture. Those at the market for the first time are the least likely to say they came because of price. |

|

|

Freshness and taste are a lesser concern for those visiting for the first-time compared to already established customers; yet this is still the most likely reason first-year shoppers visit the market. Rather, first year customers seem initially drawn to farmers markets for freshness and taste. As with other groups, convenience and community atmosphere are the least likely reason first-year customers frequent the market.

|

|

|

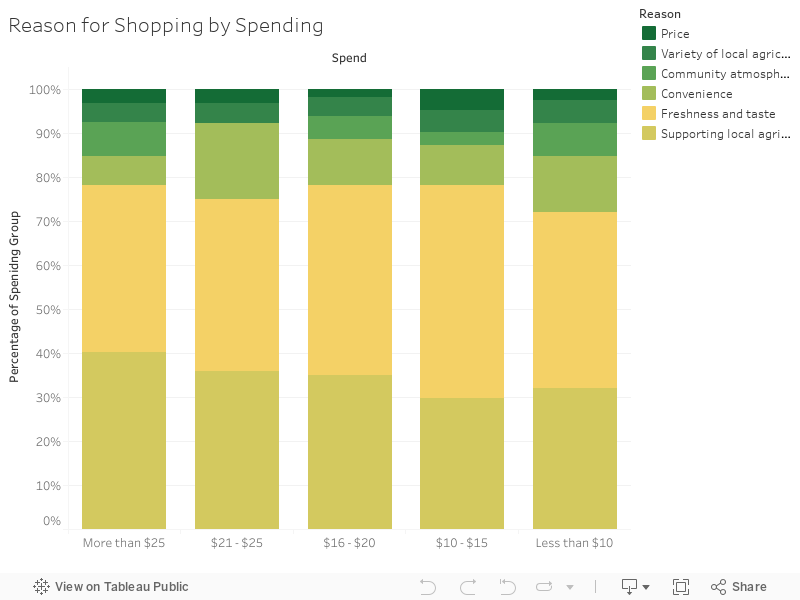

Heightened spending could be propelled with the correct types of promotion uncovered through data analysis which shows freshness and taste is not the most frequently cited reason for high spending at the farmers markets. Rather, the data show support for local agriculture is the most common reason high spending customers frequent farmers’ markets. Still, the least cited reasons for frequenting the market mirror those of other shopper groups; price and variety.

|

|

|

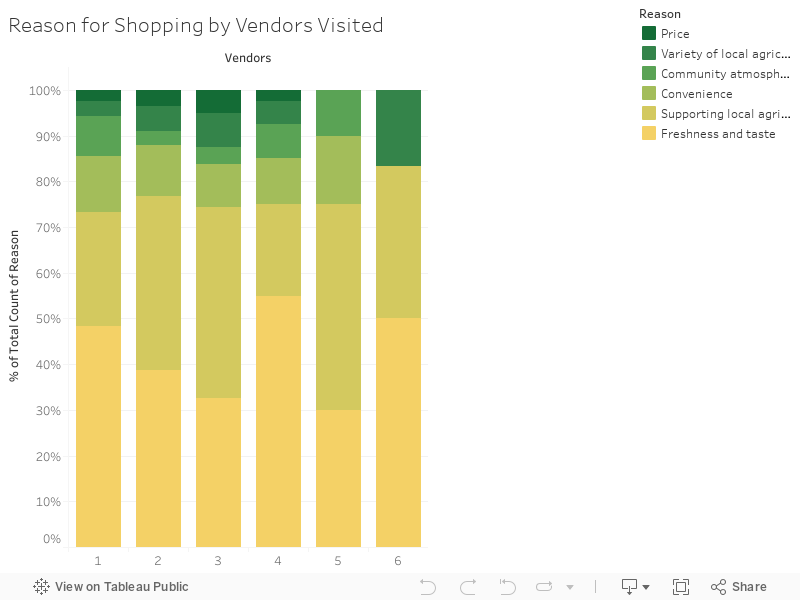

Generally, the more vendors respondents visit the more likely they are to cite freshness and taste as the reason for shopping at farmers markets, followed closely by supporting local agriculture. Not surprisingly, those who frequent more vendors are also more likely to cite variety as their reason for shopping at the farmers market. Price however, ranks low on a list to those who frequent more vendors.

|

|

With some exceptions, customers visiting for the first time or their first season are like those who spend more money from more vendors, as they mostly seem attracted to markets to support local agriculture. However, freshness and taste are also heightened a concern, which could likely be folded into promotion efforts that also highlight support for local farmers and their products. Price and variety are cited quite infrequently as a reason for shopping at Western Southern Tier farmers markets. Similarly, price and variety are almost unanimously the least cited reasons customers visit the farmers markets. The only exception is first-year customers who are less likely than those with longer tenure to cite convenience or community atmosphere as a reason to shop at farmers markets.

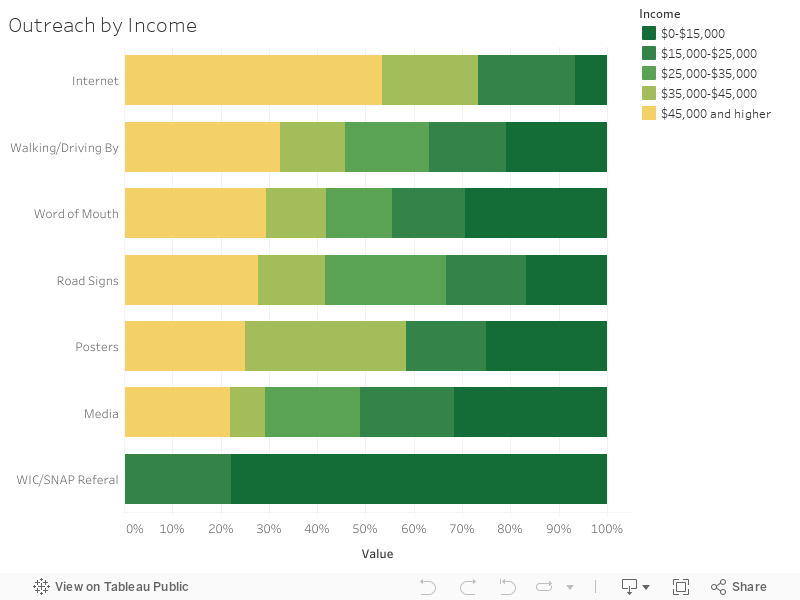

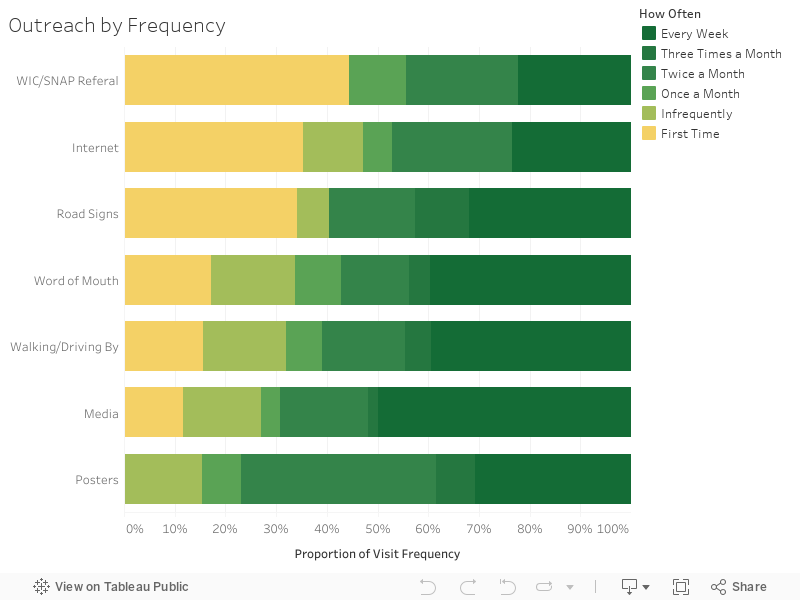

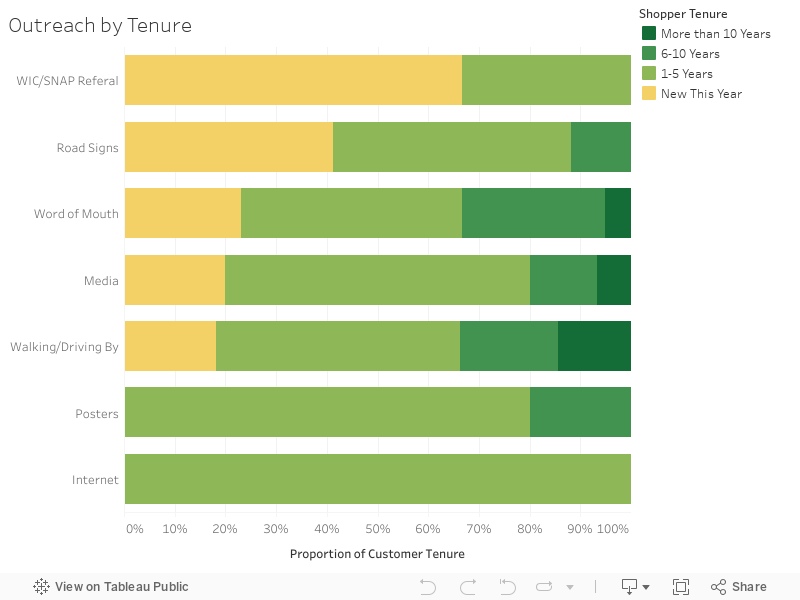

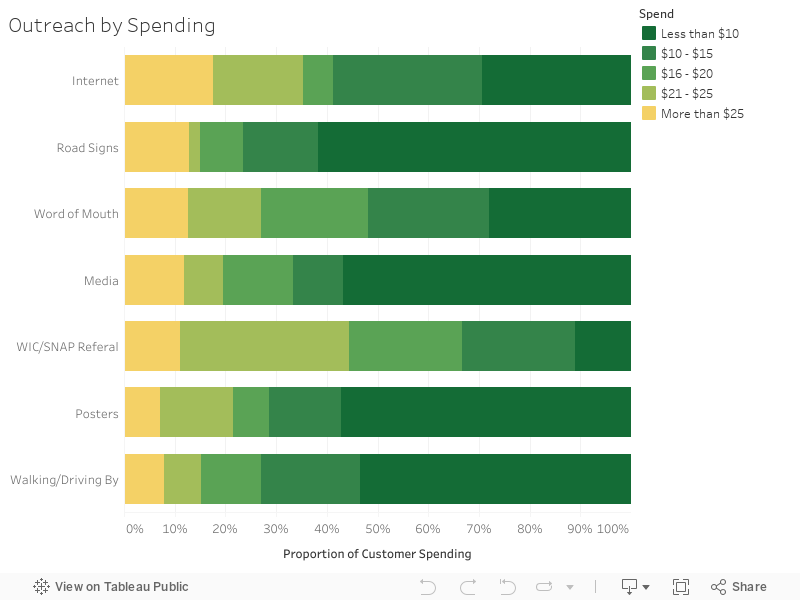

In addition to knowing what messages to promote about farmers market, the how or channels through which to distribute information is also important. Most heard about the market by simply Walking/Driving By (31.3%) or Word of Mouth (23.7%). Media (6%) and Road Signs (6%) are lesser effective means of communication, although we would need to control which markets do and do not use these means of outreach for a more accurate analysis. Almost no customers heard about the market via the Internet (2.1%) or Posters (1.7%), but again their effectiveness would depend on a control for which markets do and do not utilize these means of communication. Relatively few customers find their way to the market via WIC/SNAP referral (1.1%), an outreach strategy largely dependent upon outside factors.

Demographics

While understanding general means of promotion is important, further analysis can reveal which outreach strategies work best for young, higher-income males who are under-represented among farmers’ market customers.

While understanding general means of promotion is important, further analysis can reveal which outreach strategies work best for young, higher-income males who are under-represented among farmers’ market customers.

|

Logically, outreach to higher income customers would likely lead to more spending, with more vendors. Crosstabulation of outreach and income reveals over half of those (53.33%) who make more money are more likely to hear about the farmers market via the internet. As anticipated, no one making over $45,000 heard about the market via a WIC/SNAP referral. Media was also an ineffective means of outreach to higher income clientele.

|

|

|

Since farmers markets are mostly frequented by women, men represent an untapped customer base that could be attracted with the right types of outreach, via the right channels. While the internet is the most effective means to reach those with heightened incomes, men are more likely to hear about the market via the media than other means, or by posters. Men are least likely to hear about the market via a WIC/SNAP referral or the internet—the latter of which is in complete contrast the ways higher-income patrons hear about the market.

|

|

|

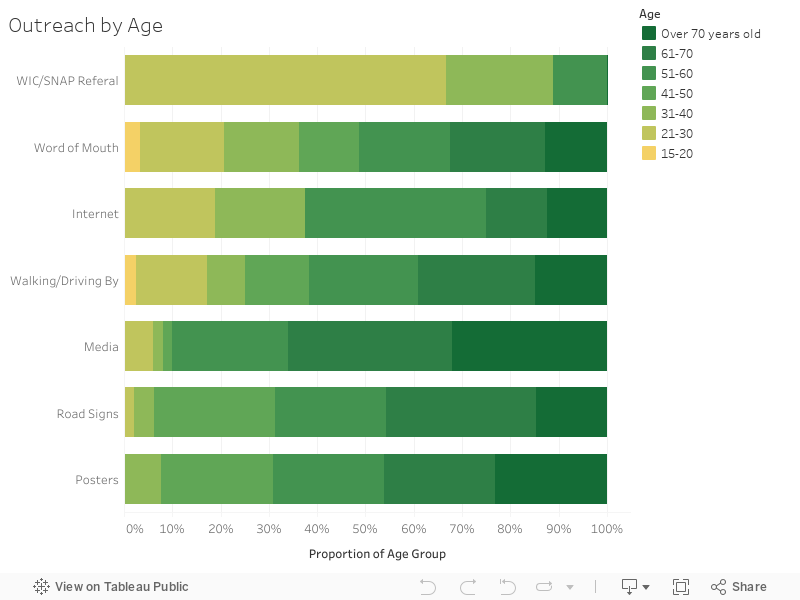

With an aged clientele, markets should concern themselves with attracting younger customers. With so few older respondents coming to the market because of a WIC/SNAP referral, the data can appear to show this is an effective outreach strategy. Still, since this likely a function or program eligibility, it would likely be more accurate to conclude there is a relationship between a younger age and coming to the market via word of mouth or the internet. In turn, posters and road signs are the least effective outreach means for younger customers.

|

|

Unfortunately, there is no single outreach means to recruit the young, higher-earning men to the farmers market. Still, the data show internet outreach can effectively reach both those who are younger and those who make more money, and thus that might be a means markets could consider utilizing more often.

Shopping Patterns

Just as outreach strategies can be analyzed across demographic groups, crosstabulation with ideal shopping patterns can also guide future outreach to recruit customers who spend more with more vendors from a pool of clients attending for their first time, or during their first year.

Just as outreach strategies can be analyzed across demographic groups, crosstabulation with ideal shopping patterns can also guide future outreach to recruit customers who spend more with more vendors from a pool of clients attending for their first time, or during their first year.

|

Knowing how first-time visitors found their way to market could help attract more newcomers. Those coming for the first time most likely heard about the market via a WIC/SNAP referral or the internet. No first-time visitors came to the market via posters and only 11.5% heard about the market via the media.

|

|

|

Similar to first time customers, knowing what brought first-year customers to the market might also recruit new visitors. The largest proportion of customers coming for the first year heard about the market from a WIC/SNAP referral, followed by road signs. No first-year shoppers heard about the market through posters or the internet.

|

|

|

In some respects, higher-spending customers might be the group markets should seek out above all others. Somewhat contrary to logic, shoppers spending more than $20 were most likely to hear about the market via a WIC/SNAP referral, followed by the internet. Higher spending customers were unlikely to hear about the market via road signs or simply by walking/driving by.

|

|

|

Customers who visit more vendors are more likely to hear about the farmers market by internet or word of mouth. Those customers who visit fewer vendors are more likely to hear about the market via road signs or walking/driving by.

|

|

While not the most effective means to outreach to all groups, the internet is an effective means to reach customers coming their first year who also spend more money, with more vendors. Generally, road signs and media are less useful strategies to recruit customers with idea shopping habits.

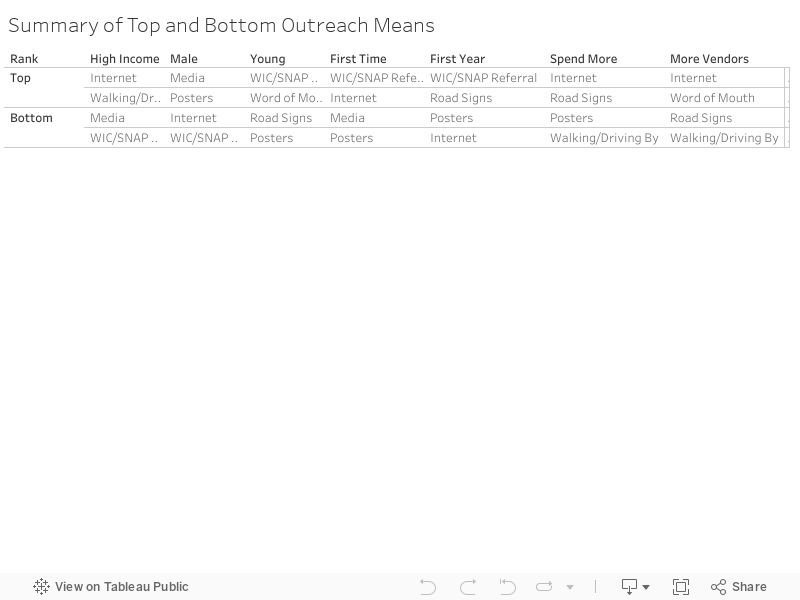

Looking across demographics and shopping patterns at the top and bottom two outreach strategies, the internet and WIC/SNAP referrals emerge as the most effective means to reach young, high-income men who spend more from more vendors, which are drawn from the pool of first-time and first year customers. In turn, posters and road signs are the least effective outreach means to customers in ideal demographic groups who display the most beneficial shopping behaviors.

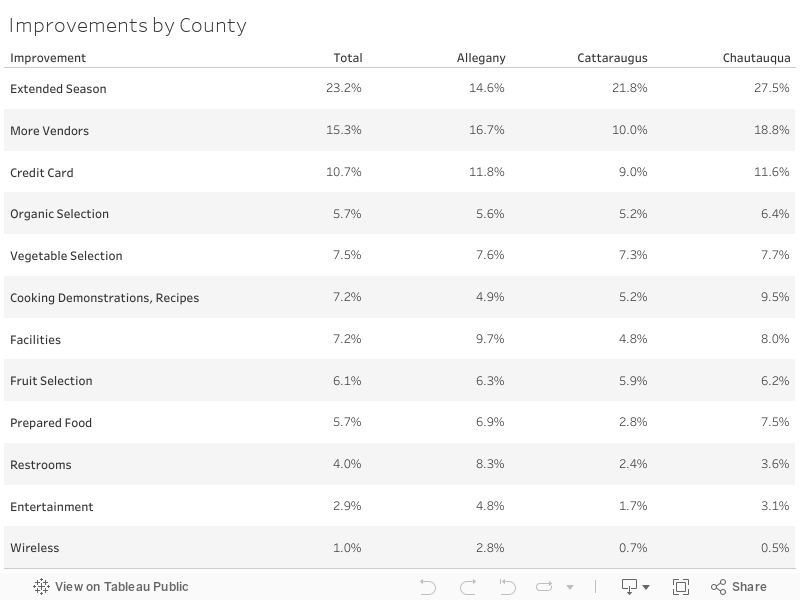

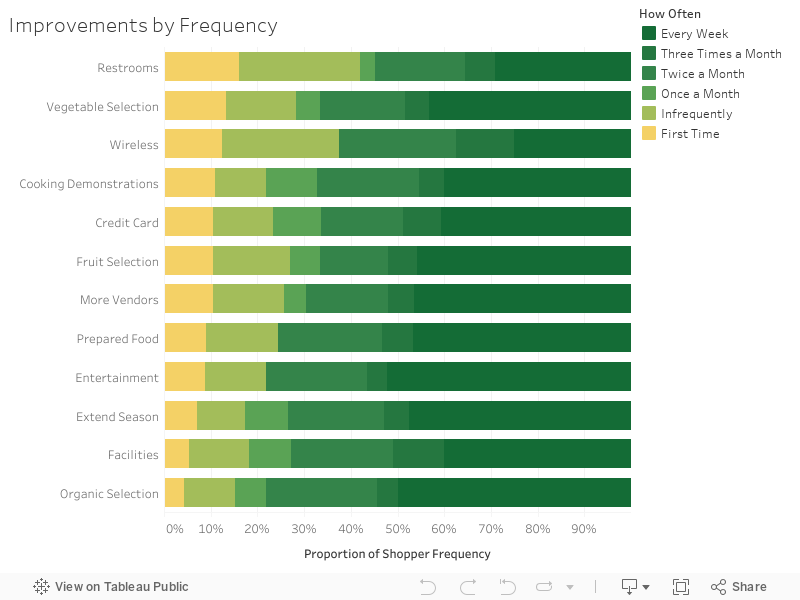

Customers were asked about what could improve local markets. The largest percentage asked for an extended season, more vendors, and the ability to pay with credit cards. Access to wireless internet and entertainment are the least cited improvements markets could make. Like purchases, promotion, and outreach this data can be cross tabulated with demographics and shopping patterns—including income.

|

Demographics

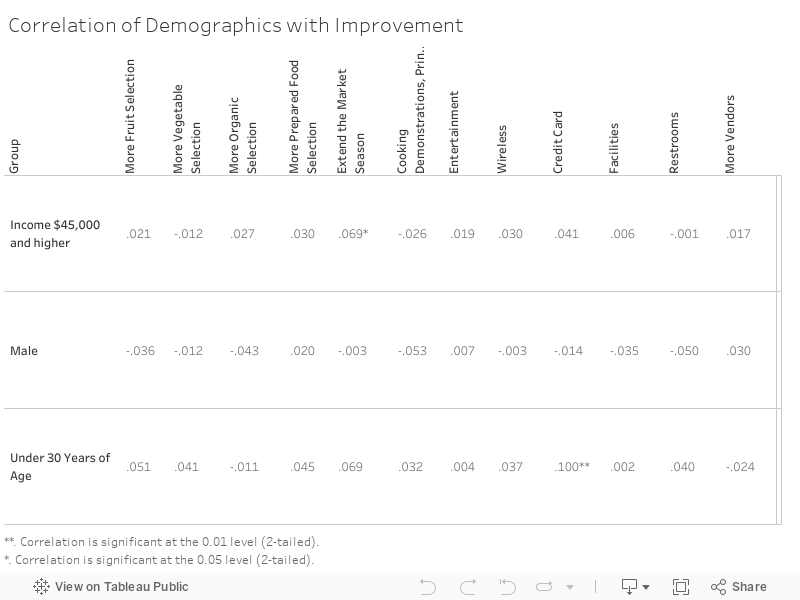

Given that farmers markets in The Western Southern Tier serve mostly those with limited means, there is room to expand the customer base into higher income clientele by making the improvements this group calls for. Those in the top income bracket ($45,000 and above) were more likely than others to say wireless internet access would improve the market—the lowest cited improvement amongst all customers. Prepared foods and an extended season may also be effective strategies to draw in higher income customers. In contrast, higher income customers see little need for cooking demonstrations and appear satisfied with the current vegetable offerings. |

|

|

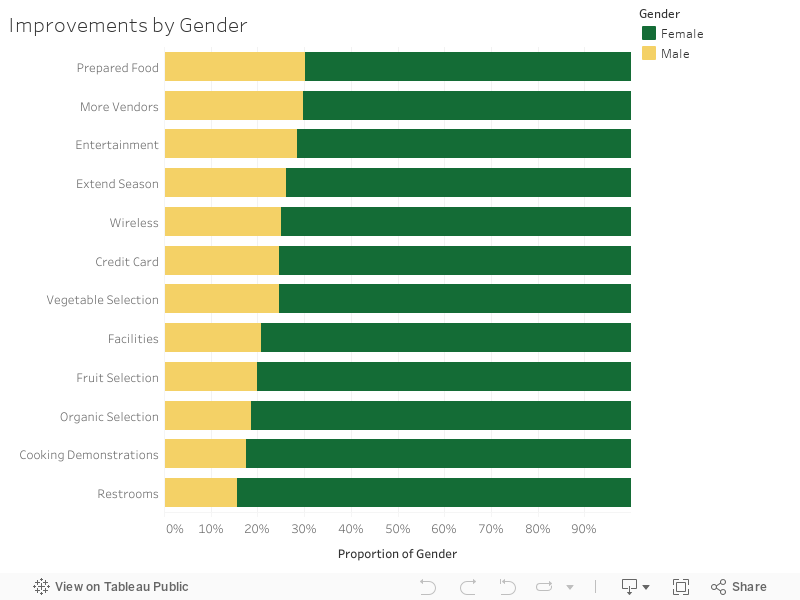

Markets might be able to almost double their customers with improvements that would draw more men. Men, more so than women think farmers markets could be improved by offering more prepared foods and more vendors more generally—which according to the data, would entail more vegetables, fruits and organics in that order. Men are much less likely than women to think cooking demonstrations or restrooms would improve markets.

|

|

|

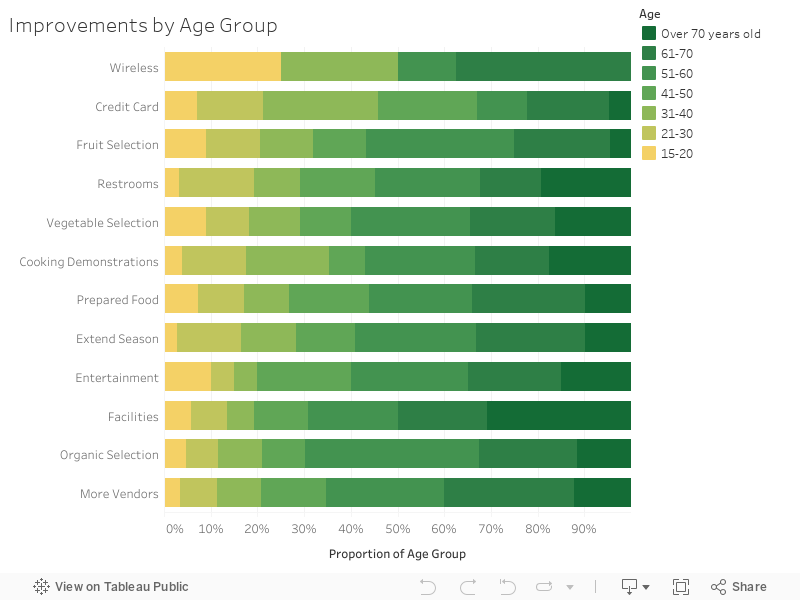

The right types of improvements could translate into a younger customer base who would then have the most potential to turn into long-term customers. Customers under thirty years of age are more likely than older customers to ask for wireless internet access and credit card processing than older customers. Younger customers seem pleased with the organic selection and amount of vendors farmers markets in The Western Southern Tier offer.

|

|

Overall, the data point to wireless internet access as the most effective improvement needed to attract young, high-income men to farmers markets. However, given the expansion in mobile internet service since the survey was administered, this may no longer be necessary. Yet at the same time, no other improvement was fitting across target demographic groups. In turn, the least called for improvement by young, high-income men was for cooking demonstrations.

|

Shopping Patterns

Data-driven improvements might be one of, if not the best way to ensure first time visitors turn into long-time customers. Restrooms and an expanded vegetable selection are the most common improvements mentioned by those visiting farmers markets for the first time. While first time customers call for restrooms; they are unlikely to ask for other types of facilities and they seem satisfied with current organic offerings. |

|

|

Like first-time visitors, the right types of improvements could turn those coming for their first season into long-term customers. Similar to first time visitors, first-year customers’ most common suggestion for improvement are restrooms—and similar to first-time visitors who call for an expanded vegetable selection, those shopping in the first-year call for an expanded fruit selection. In turn, no first-year customers called for wireless access, entertainment, more facilities or an expanded organic selection.

|

|

|

To enhance the bottom line, small improvements for a few high-spending customers might be equivalent to immense improvements for a larger number of small-spenders. Those spending more ask for restrooms and credit card processing more than any other improvement. In turn, high-spending customers seem pleased with the current facilities and availability of prepared foods.

|

|

|

While maximizing customer numbers would benefit markets; they could also be enhanced by ensuring customers also frequent more vendors. The data show there is a relationship between frequenting more vendors and wanting improved facilities, including restrooms. In contrast, there is a negative relationship between vendors visited and a desire of wireless access and of course, more vendors.

|

|

The top and bottom two improvements across underserved demographic groups and customers with idealized behaviors reveal the most, and least desired things markets could do to attract these types of shoppers. While a very uncommon request by men, a common improvement suggested across the most sought-after customers are restrooms. The next common improvement called for was wireless internet access, although expanded alternatives since the surveys were administrated may have caused this suggestion to atrophy. While restrooms are sought, other facility improvements are not. Similarly, customers with ideal demographic traits and behaviors seem content with current offerings of organics and do not see a need for cooking demonstrations.

Like many rural communities, a slowly unfolding and still ongoing shift into a postindustrial economy pushed the once prosperous Western Southern Tier of New York State into a region plagued by rural poverty and its associated problems—including decades of outmigration that leaves behind a largely poor, female and aged population. In this context, farmers markets are a way to stimulate economic activity while simultaneously providing healthy foods to marginalized populations. This report utilizes shopper demographics and behaviors to expand market customer bases.

Demographics

Given the regional demographics, it is hardly surprising most farmers’ markets customers in the region are low-income women of accelerated age. Still, in comparing these shopper attributes to county demographics, we still see room for markets to expand into a potential pool of men under the age of thirty who make more than $45,000 a year. In fact, this report used a variety of cross-tabulation strategies to highlight the best means for markets to engage this potential new pool of shoppers. This strategy can be further summarized and enhanced with correlations—including correlating demographic groups with the products they purchase.

Given the regional demographics, it is hardly surprising most farmers’ markets customers in the region are low-income women of accelerated age. Still, in comparing these shopper attributes to county demographics, we still see room for markets to expand into a potential pool of men under the age of thirty who make more than $45,000 a year. In fact, this report used a variety of cross-tabulation strategies to highlight the best means for markets to engage this potential new pool of shoppers. This strategy can be further summarized and enhanced with correlations—including correlating demographic groups with the products they purchase.

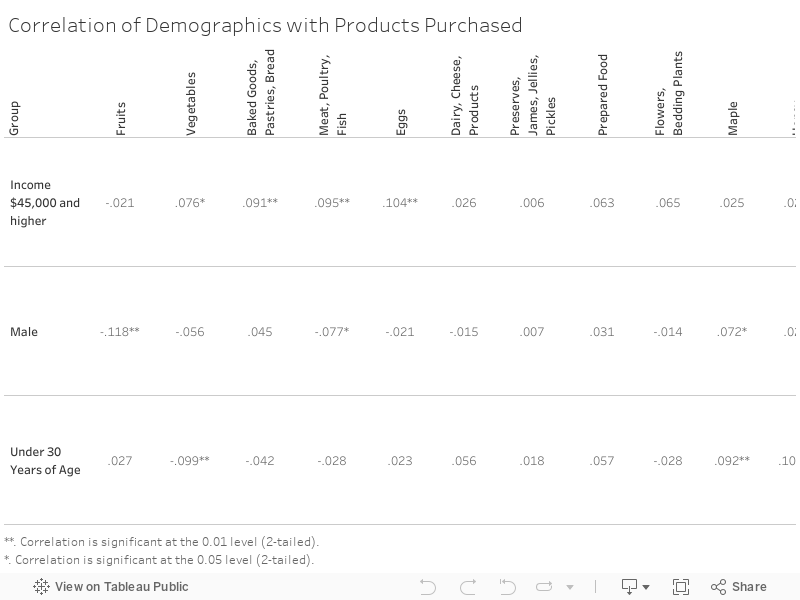

The data reveals those with heightened incomes are significantly more likely than those who make less than $45,000 to purchase vegetables, baked goods, meat, eggs and crafts. Men are significantly less likely than women to purchase fruits and meat; but more likely to purchase maple. Those under thirty are also significantly more likely than older customers to purchase maple, along with honey, cider/judice and packaged foods. In turn they are significantly less likely than older customers to purchase vegetables.

|

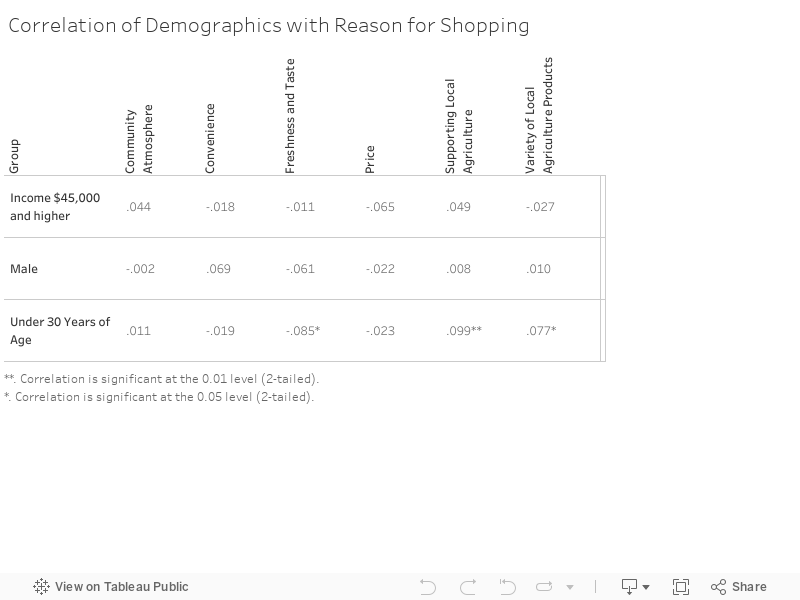

Correlations of the reason for shopping and demographic reveals no significant relationships with income or gender. However, those under 30 years of age are significantly more likely than older customers to support local agriculture and significantly less likely to shop for freshness and taste along with a variety of local agricultural products.

|

|

|

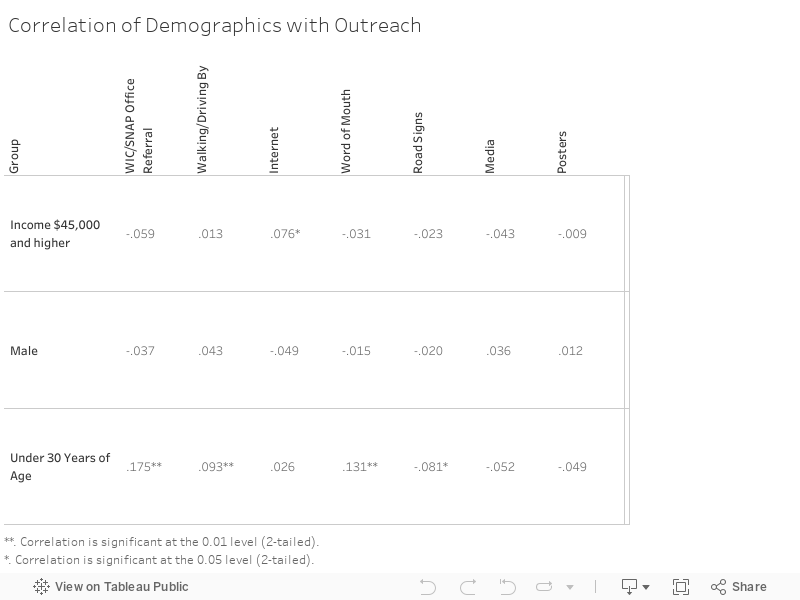

Correlations of demographics and outreach means reveal no significant relationships with gender. However, the correlations also reveal those with incomes of $45,000 and above are more likely than those who make less to hear about the market via the internet. Young customers are significantly more likely than those over 30 years of age to hear about the market via a WIC/SNAP office referral, walking or driving by, or word of mouth. Younger customers are significantly less likely to hear about the market via road signs.

|

|

The correlations of suggested improvements and demographics reveal no significant relationships with gender. However, those making more than $45,000 are significantly more likely than those who make less to think the market season should be extended. Those under the age of thirty are significantly more likely to request the ability to pay with credit cards compared to older customers.

Shopping Patterns

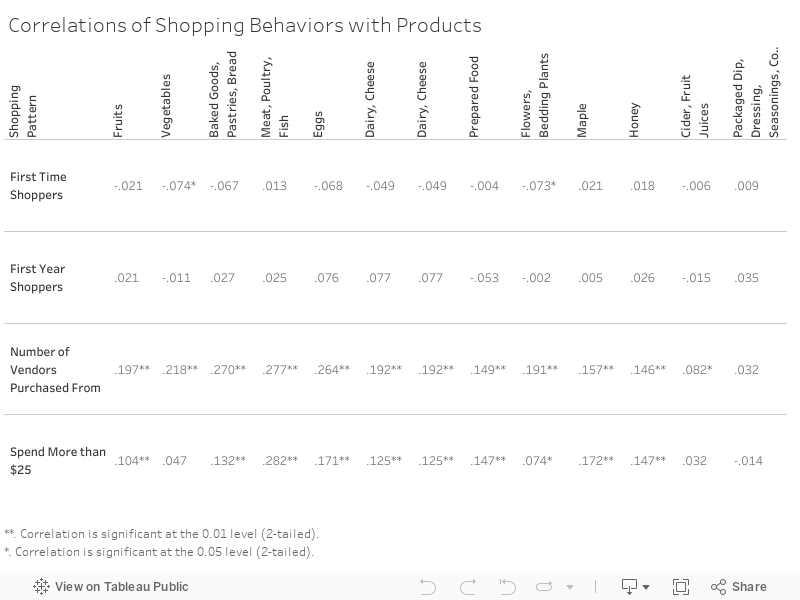

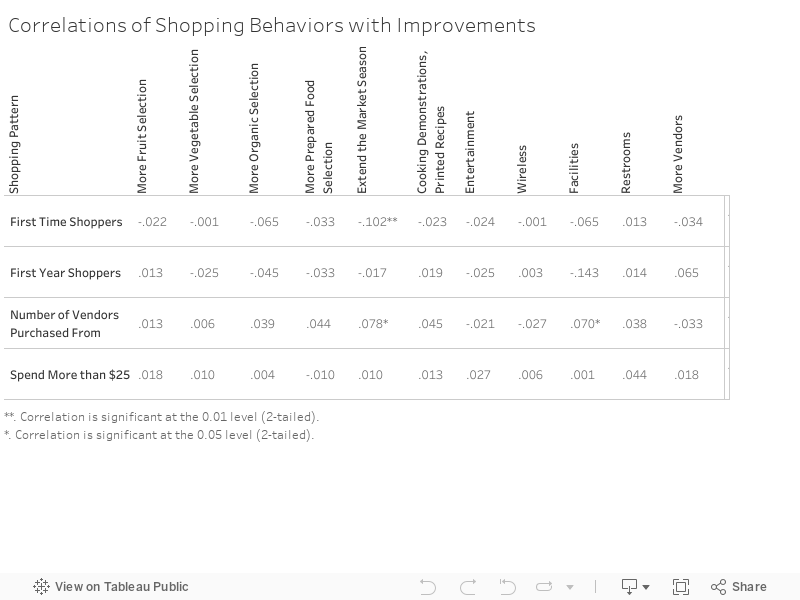

Shopping behaviors can also be correlated with other indicators, including the products purchased. This calculation reveals no significant relationships with first year shoppers; and logically most products are significantly correlated with the number of vendors frequented and the higher spending. First time shoppers are significantly less likely to purchase vegetables and flowers; there is nothing they are significantly more likely to purchase.

Shopping behaviors can also be correlated with other indicators, including the products purchased. This calculation reveals no significant relationships with first year shoppers; and logically most products are significantly correlated with the number of vendors frequented and the higher spending. First time shoppers are significantly less likely to purchase vegetables and flowers; there is nothing they are significantly more likely to purchase.

|

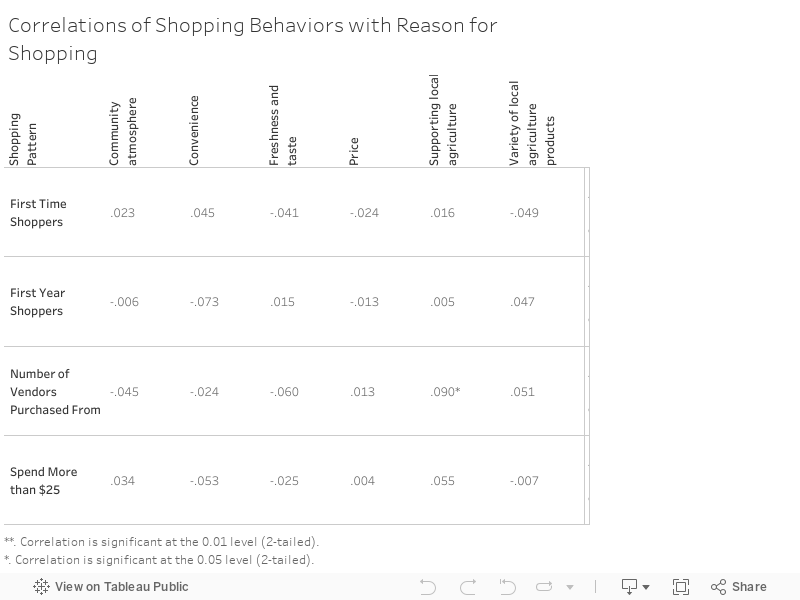

There are no significant correlations with first time shoppers, first year shoppers or spending with the reasons for frequenting the market. However, those who frequent more vendors are significantly more likely to say they shop at the farmers market to support local agriculture.

|

|

|

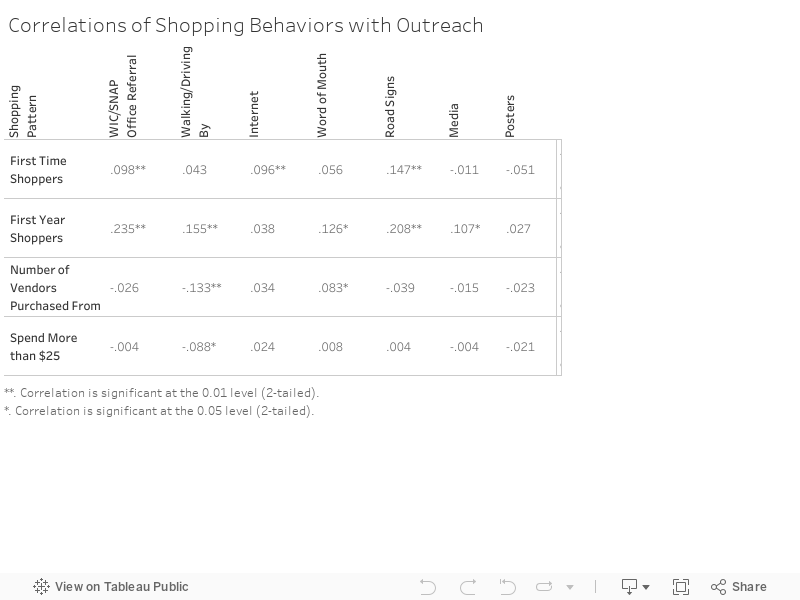

Correlations reveal first time and first year shoppers are significantly more likely to hear about the market via a WIC/SNAP referral, the Internet or Road Signs. Additionally, first year shoppers are significantly more likely to heard about the market by walking or driving by than those with longer tenure. In contrast, those who shop at more vendors, along with those who spend more than $25 are less significantly less likely to hear about the market by walking of driving by. Rather, those who buy from more vendors are more likely to hear about the market via word of mouth.

|

|

There are no significant correlations with spending nor first year shoppers and calls for improvement; although first time shoppers are significantly less likely to recommend extending the market season. The number of vendors frequented is correlated with calls to extend the market season, along with an improvement of facilities.

Discussion

Surveys across The Western Southern Tier reveal the ways in which farmers markets can better cater to both underserved customers and those with idealized shopping behaviors. Still, the results in this report are not without their shortcomings. A primary concern is aggregating across markets; as each individual market should assess itself, in the context of its local community before undertaking any significant changes. Similarly, the general strategy utilized in this report in regards to tapping a large, underserved customer base may not be applicable to all markets who instead, might want to improve services to the existing customers they have already secured.

Surveys across The Western Southern Tier reveal the ways in which farmers markets can better cater to both underserved customers and those with idealized shopping behaviors. Still, the results in this report are not without their shortcomings. A primary concern is aggregating across markets; as each individual market should assess itself, in the context of its local community before undertaking any significant changes. Similarly, the general strategy utilized in this report in regards to tapping a large, underserved customer base may not be applicable to all markets who instead, might want to improve services to the existing customers they have already secured.

Fresh Local WNY is a sponsored project of Southern Tier West RP&DB

CONTACT USSouthern Tier West RP&DB

Kimberly LaMendola Regional Economic and Food Systems Development Manager [email protected] Phone: 716-945-5301 Ext. 2211 |

|

© 2024 Southern Tier West Regional Planning & Development Board